Most small businesses treat expense variances like speed bumps—something you notice, slow down for, then immediately forget. You run the monthly reports, see marketing overspent by 23%, facilities came in under by $4,000, payroll hit exactly on target. Everyone nods during the review meeting, promises to "keep an eye on it," and nothing actually changes until year-end when you're scrambling to explain why you're 40% off budget.

The problem isn't the variance reporting itself. It's that variance reports don't automatically trigger anything. They're observations without obligations, measurements without mechanisms.

Companies that turn variances into reforecast triggers end up with budgets that actually mean something by Q3. The ones that don't are still running on January's budget in October, wondering why nothing lines up.

The expense-to-budget mapping mess

What expense-driven reforecasting actually looks like in most small businesses: expenses come through five different systems—credit cards, ACH payments, manual checks, Venmo for that one vendor who refuses to modernize, and petty cash that somehow still exists. Each transaction hits your books with whatever description the vendor decided to use that day. "AMZN MKTP US*2Y4" could be office supplies, could be that industrial printer, could be holiday decorations.

Your budget, meanwhile, sits in a completely different universe. Marketing has a line item for "Digital Advertising" budgeted at $8,000 monthly. But the actual charges come through as:

-

FB *ADVERTISING ($2,847)

-

GOOGLE ADS ($3,200)

-

LinkedIn Marketing Sol ($890)

-

Canva Pro ($45)

-

Some random charge from "STRIPE PAYMENT" that turns out to be your email marketing tool ($299)

Without proper mapping, you're comparing apples to alphabet soup. The finance team spends hours every month manually categorizing expenses, usually after the fact, which means your variance reports are always looking backward instead of forward.

Setting variance thresholds that actually trigger action

Most businesses set variance thresholds like they're picking lottery numbers. "Let's say 10% triggers a review." Why 10%? Because it sounds reasonable. But a 10% variance on a $500 office supplies budget is meaningless noise, while a 10% variance on $80,000 monthly payroll is a massive flag.

Stop losing track of your business spending.

Costyly helps you record, monitor & control expenses—accurately and efficiently.

- Automated expense categorization

- Real-time budget tracking

- Detailed financial reports

No credit card required

Thresholds need three dimensions, not one.

Percentage variance matters for proportional control. A 50% spike in any category deserves attention regardless of absolute size.

Dollar variance catches the big movers. Even a 5% variance on a $100,000 line item means $5,000—that's real money that doesn't show up as alarming on a percentage basis.

Consecutive variance identifies trends. Marketing overspending by 8% once might be a campaign timing issue. Three months in a row? That's a broken budget.

A threshold matrix that actually works:

| Budget Category | Monthly Budget Range | % Trigger | $ Trigger | Consecutive Months |

|---|---|---|---|---|

| Payroll | $50k–$200k | 5% | $5,000 | 1 |

| Marketing | $5k–$20k | 15% | $2,000 | 2 |

| Operations | $10k–$40k | 10% | $3,000 | 2 |

| Facilities | $8k–$15k | 20% | $2,500 | 3 |

| Admin/Supplies | <$5k | 25% | $1,000 | 3 |

The consecutive month trigger prevents overreacting to timing differences while catching real trends before they compound into something harder to fix.

Who owns what: the responsibility matrix nobody wants to create

Variance without ownership is just expensive data collection. Every threshold breach needs a specific person who receives the alert, investigates the cause, and decides on action—not a committee, not "the finance team," but an actual human with a name and email address.

The typical dysfunction looks like this: Finance notices marketing overspent. They email the CMO, who forwards it to their team lead, who asks the coordinator to look into it. Two weeks later, after three follow-ups, you discover it was a prepayment for an annual conference that should've been amortized. Meanwhile, the real problem—rising customer acquisition costs—goes completely unnoticed because everyone was playing email hot potato.

Building your ownership matrix means defining four roles for every category:

Primary Owner: The budget holder who approved the original budget

Investigator: The person closest to the actual spending (often different from the owner)

Approver: Who can authorize a reforecast if needed

Stakeholders: Who needs to know about changes (usually more than you think)

Route alerts directly to people who can actually answer the "why."

For a marketing overspend, that might look like: Primary Owner is the CMO, Investigator is the Marketing Operations Manager, Approver is the CFO (for reforecasts over $5k monthly impact), and Stakeholders include the CEO, Sales Director, and Finance Manager.

The investigator role is critical and almost always missed. The CMO doesn't know why Facebook ads cost 30% more this month—their performance marketing manager does. Route alerts directly to people who can actually answer the "why."

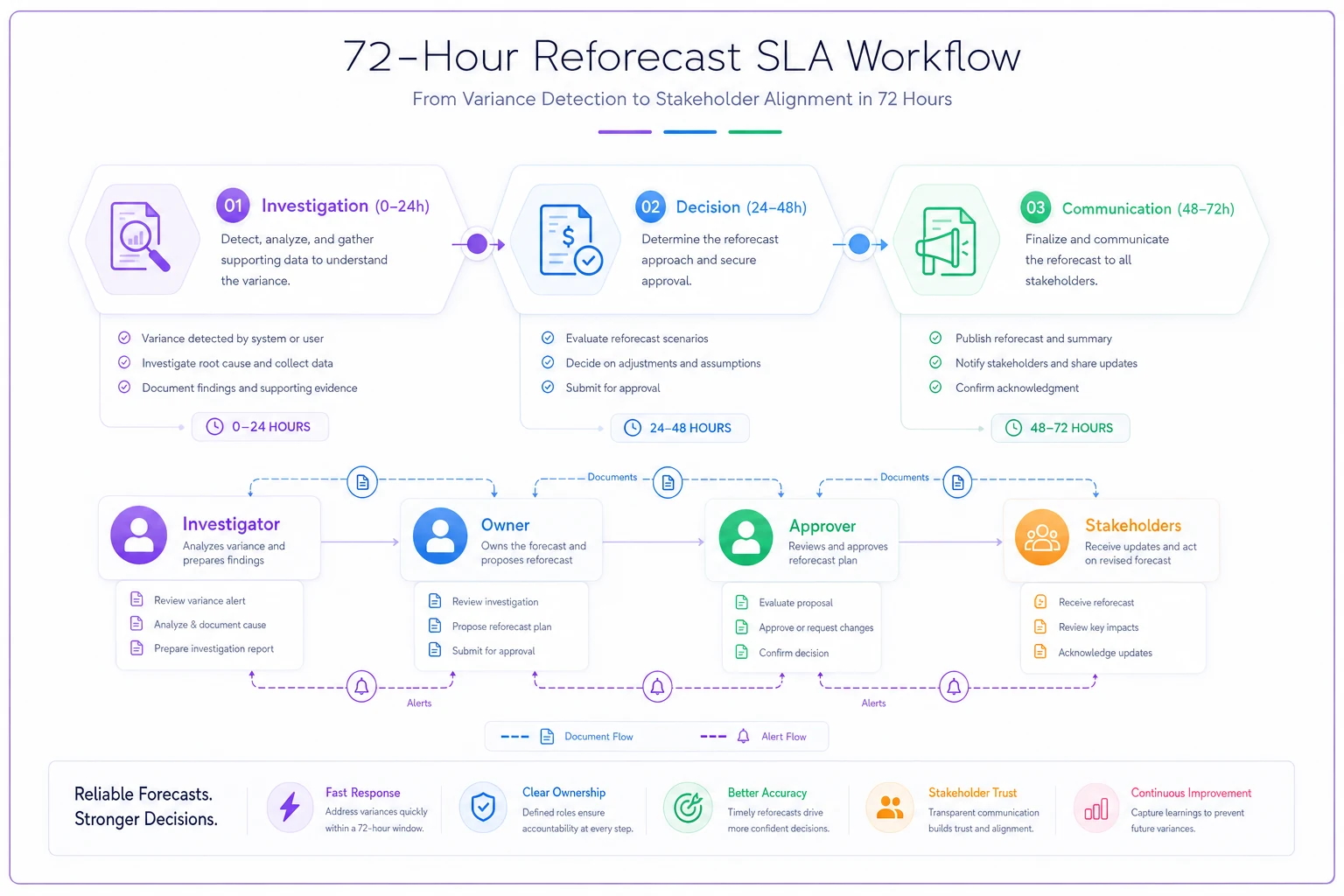

From variance to reforecast: the 72-hour SLA

When a variance triggers, most companies enter analysis paralysis. They schedule meetings to discuss scheduling meetings about the variance. By the time any decision gets made, you're halfway through the next month.

A 72-hour reforecast SLA changes that. The process runs in three stages:

-

Hour 0–24

Investigation.

The investigator pulls transaction details, identifies the variance driver, and determines whether it's a timing issue that will self-correct, a one-time event that won't repeat, or a structural problem that will continue or worsen. -

Hour 24–48

Decision.

Based on the investigation, the owner decides: no action needed (document why), adjust this month only, reforecast remaining months, or request budget reallocation. -

Hour 48–72

Communication.

Update the forecast model, send a standardized notification to stakeholders, document in the variance log, and adjust any dependent budgets.

This sounds aggressive until you realize the alternative is discovering in November that you've been trending 20% over budget since May.

This diagram shows the roles and steps in the 72-hour SLA workflow.

This sounds aggressive until you realize the alternative is discovering in November that you've been trending 20% over budget since May.

The variance alert that actually drives action

Generic variance alerts train people to ignore them. "Marketing is 12% over budget" tells you nothing actionable. Compare these two:

Bad Alert: Subject: Budget Variance Alert - Marketing Marketing expenses exceeded budget by $1,847 (12%) in October.

Actionable Alert:

Subject: ACTION REQUIRED: Marketing overspend requires reforecast decision by Thursday October Marketing Variance: +$1,847 (+12%) Driver: Google Ads CPC increased from $3.20 to $4.15 (+30%)

-

Competitive bidding in primary keywords

-

No corresponding conversion rate improvement

Impact if continues: $22,164 annual overspend

Required Decision by Thursday 5pm:

-

Reduce ad spend to stay within budget (est. -15% lead volume)

-

Reforecast marketing up $1,800/month (requires offset from other departments)

-

Shift budget from events (-$2,000) to digital (+$2,000)

Previous variances: None in last 6 months Owner: Sarah Chen Investigator: Mike Torres

The second alert creates urgency, provides context, shows downstream impact, and presents clear options. It demands a specific decision by a specific time—hard to file away and forget.

Sample journal entries: making reforecasts real

Most reforecasts die in spreadsheet purgatory. The budget gets updated in the planning tool, maybe someone updates a dashboard, but the actual financial system generating your reports? Still running on January's numbers.

When you reforecast, you need journal entries that actually flow through your system:

Scenario: Marketing reforecast from variance Original October budget: $15,000 Actual October spend: $17,500 Decision: Reforecast +$2,000 monthly for Q4 Journal Entry (October 31): DR: Marketing Expense - Digital Advertising $2,500 CR: Budget Variance - Marketing $2,500 (To record October overspend against budget) DR: Budget Reforecast - Marketing Q4 $6,000 CR: Contingency Reserve $6,000 (To formally reforecast Q4 marketing budget)

This creates an audit trail showing not just that you overspent, but that you made a conscious decision to reforecast rather than reduce spending. Come year-end, you can trace every reforecast decision back to its triggering variance.

What breaks when you scale past 50 employees

Small variance management systems that work for 20-person companies implode somewhere around 50 employees. Suddenly multiple people are charging to the same budget categories, expense categories mapped to your chart of accounts becomes a full-time job, and that simple threshold matrix turns into a 200-row spreadsheet nobody maintains.

The breaking points are predictable.

Categorization delays compound. With 5 credit cards, miscategorized expenses are annoying. With 50 cards across 10 departments, you're burning 20 hours a month just cleaning up coding before you can run variance reports.

Threshold fatigue kicks in. At first, investigating every variance over $1,000 makes sense. Six months in, when you're getting 30 alerts monthly, people start treating them like spam.

Ownership confusion multiplies. When marketing was three people, everyone knew Sarah owned the budget. Now marketing is 12 people across paid media, content, events, and partnerships. Who investigates when the department goes over?

Reforecast authority conflicts emerge. One director reforecasting a $15k budget is fine. Five directors wanting to reforecast simultaneously with only $20k in contingency left? Now you need a process for prioritizing competing requests—and someone willing to say no.

How AI-powered platforms handle the heavy lifting

This is where operational software starts carrying real weight. Instead of manually mapping every transaction, AI automation can learn that "AMZN MKTP" transactions under $100 are office supplies while anything over $500 is probably equipment. Recurring patterns get discovered automatically, so that monthly Salesforce charge stops catching people off guard.

Variance monitoring happens continuously instead of monthly. As transactions flow in, they're categorized, matched against budget lines, and checked against thresholds. When something trips a threshold, the alert routes directly to the assigned investigator with transaction-level detail already attached—no digging required.

More importantly, reforecast decisions get documented and pushed across connected systems. Update the forecast in one place and it flows through to your reporting, your KPI dashboards, and your variance thresholds for next month. Journal entries generate automatically with proper audit notes.

The goal isn't removing human judgment—it's removing the manual work that prevents people from exercising that judgment quickly enough to matter.

The patterns that predict reforecast needs

Certain patterns reliably signal future reforecasts before the numbers fully break.

Creeping vendor increases. When multiple vendors in the same category raise prices within 60 days of each other, the budget is already toast. Web hosting, email platform, and CRM all announcing 10–15% increases isn't getting absorbed—that's a structural change requiring reforecast.

New hire ripple effects. Everyone budgets for salary and forgets the rest. A new senior developer doesn't just cost $120k. They need a laptop, software licenses, possibly travel budget, definitely more AWS capacity. Fully-loaded cost typically runs 30–40% above salary, and it hits different budget lines at different times.

Seasonal compression. Businesses with seasonal patterns consistently underbudget the slow months. If 40% of revenue comes in Q4, expenses don't drop 40% in Q1—maybe 15% at best. The fixed cost base creates larger percentage variances that trigger false alarms unless you build seasonality directly into your thresholds.

Contract renewal clustering. Companies tend to sign annual contracts in clusters—January and July are popular. When seven software contracts all renew in the same month, even with modest 5% increases each, the cumulative hit blows through monthly thresholds.

When reforecasting is the wrong answer

Not every variance should trigger a reforecast. Sometimes the right response is forcing spending back in line. The distinction matters because reforecasting too easily teaches the organization that budgets are suggestions.

Don't reforecast when it's clearly controllable spending—the team went over the entertainment budget because they decided on an expensive steakhouse dinner. That's a spending control issue, not a reforecast situation. Similarly, if you prepaid an annual software license that usually gets paid monthly, the variance self-corrects over the year. Document it and move on.

Watch out for reforecasting as a way to avoid hard decisions. If marketing keeps missing acquisition targets despite increased spending, reforecasting just enables the problem. Sometimes the answer is forcing efficiency improvements, not providing more budget.

And if the money doesn't exist, reforecasting is reallocation, not magic. If everyone's over budget and there's no contingency left, something has to give. Reforecasting without identifying a funding source just pushes the problem to December.

Building your reforecast capacity

Most small businesses treat reforecasting like an emergency procedure—something you do when things go really wrong. Building it into your normal operational rhythm changes that entirely.

Start with a contingency reserve that's actually accessible. Not the "board-approved emergency fund" requiring three signatures and a presentation to touch. Operating contingency should be roughly 5–8% of monthly operating expenses, available at the CFO or controller level, specifically for reforecast needs.

Keep a reforecast log that tracks the original trigger, investigation findings, decision made, approval obtained, impact on annual budget, and actual vs. reforecasted results. This historical data becomes genuinely useful for improving thresholds and separating signal from noise over time.

Set a reforecast review cadence—monthly is too reactive, annually is pointless. Quarterly works for most businesses. Look at all reforecasts made, identify patterns, and adjust your base budgets for the following year. If you're constantly reforecasting marketing up 20%, the base budget is wrong.

The bottom line on expense-driven reforecasting

Expense variance reports without reforecast mechanisms are like smoke detectors without sprinkler systems—they tell you there's a problem but don't help you fix it. The businesses that stay ahead of their numbers build systems where variances automatically trigger investigation, investigation drives decisions, and decisions update forecasts before the damage compounds.

The key isn't perfecting thresholds or building elaborate approval matrices. It's creating a mechanical connection between noticing a variance and actually doing something about it within 72 hours. That requires clear ownership, documented processes, and—increasingly—software that handles the pattern matching and alert routing without someone manually pulling it together each month.

Small businesses that implement expense-driven reforecasting tend to see meaningful improvement in budget accuracy by year-end. More importantly, they stop getting blindsided in December by problems that started in April.

Your budgets are either living documents that evolve with reality, or they're January's best guess that everyone stops looking at by June. The reforecast system you build determines which one you get.

Expense variance reports without reforecast mechanisms are like smoke detectors without sprinkler systems—they tell you there's a problem but don't help you fix it.

Ready to master your business expenses?

Join 5,000+ businesses using Costyly to save time, reduce overspending, and improve financial visibility.